Sending money abroad from India seems like a straightforward process until you hit unexpected snags.

Whether it’s for funding overseas education, sending gifts, or transferring funds to your close ones, some mistakes can complicate your international remittance. These errors can slow down your transfer, reduce the amount your recipient gets, or worse, lead to transaction rejection.

In this article, Robint, our head of “International Remittance,” draws from his personal experience the 8 mistakes he has seen people make when sending money abroad.

“This article is not just about avoiding money transfer mistakes; it’s also about ensuring your money reaches its destination as intended, with every aspect, from beneficiary information to transaction details, handled with care. So let’s get started.” – Robint.

8 Money Transfer Abroad Mistakes To Avoid

1. Not Linking PAN & Aadhar

The government has made it mandatory for PAN & Aadhar to be linked. The deadline for this was on June 30, 2023. If this has not been done, then as per government rules you cannot do money transfers abroad from India. Robint says “While most people have already linked their PAN & Aadhar, we still get some cases where this hasn’t happened and we inform the customer to do the same”.

Consequence: Transaction on hold till compliance is achieved

During the KYC verification process itself your transaction will be flagged and not proceed further. If you need to transfer funds abroad for your child’s education, like paying their university fees, this delay could derail those plans as these payments typically need to be made within a certain date and time.

Solution: Link your PAN and Aadhar

Do it as soon as possible by visiting the government Income Tax Portal. You would have to pay a penalty of Rs 1,000 for not doing the linking yet. Once you’ve done the payment, it’ll take about 6 – 7 days for the linking to happen. Thereafter you can proceed ahead with your remittance transaction.

Also Read: PAN Aadhar Not Linked: Can You Do Any Forex Transaction?

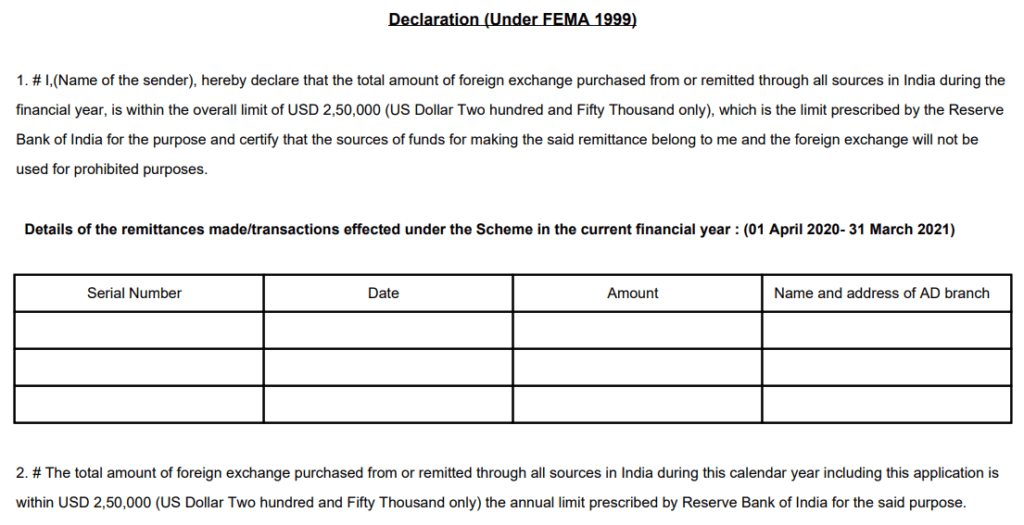

2. Incorrectly Reporting Past Forex Transactions

In Form A2, which is an application cum declaration form for doing forex transactions, there is a “Declaration Section”. Here you’ve to correctly declare the forex transactions done in the current financial year. This could be buying foreign exchange and/or doing international remittance.

The main motivation behind this declaration is that the government wants to ensure the totality of foreign exchange bought and/or transferred abroad is below USD 2,50,000 equivalent in INR. The USD 2,50,000 amount is the LRS limit (Liberalized Remittance Scheme) per resident Indian per financial year.

Consequence: Transaction on hold till compliance is achieved + legal consequences

The repercussions of inaccurately reporting these transactions can be significant. Robint recalls instances where customers claimed they had not conducted any transactions, yet a review of their PAN card transaction history revealed five or six instances within the same financial year.

Such discrepancies not only result in the necessity to pay the applicable Tax Collected at Source (TCS) but also lead to delays in transaction processing until these issues are resolved. This is a legal declaration; errors or omissions can lead to legal repercussions, including being categorized as a high-risk individual, thus subjecting future transactions to stricter compliance checks. The Income Tax or FEMA (Foreign Exchange Management Act) may impose penalties for such inaccuracies.

Solution: Accurately report the forex transactions.

The simplest and most effective solution is to report accurately the first time itself. Ensuring all past forex transactions within the fiscal year are declared correctly helps avoid legal complications and fosters transparency with financial authorities. Robint advises, “Taking the extra time to verify your past transaction details can save you from unnecessary delays and legal consequences. Always double-check your declaration in Form A2 for accuracy.

Also Read: How to Fill Form A2 For Remittance Abroad – Simple Guide

3. Not Transferring Funds From Remitter’s Bank Account

A fundamental rule in the world of international money transfers is ensuring the funds originate from the remitter’s own bank account. It is their KYC documents which are submitted at the time of KYC verification. The PAN entry for the remittance transaction is based on the given KYC and it should match the funds credited to the remitting bank’s account.

“Several times I’ve seen people make this mistake,” Robint reflects, “For example, The fund transfer for paying university fees abroad would be booked under the student’s name. However, the funds would come from the parent’s or another relative’s bank account instead of the student’s. It might seem convenient at the time to send money like this. However, this can complicate what should be a straightforward transaction”

Consequence: Transaction held in India itself. Refund initiated. Significant delay.

The funds, once identified as not matching the remitter’s KYC details, are put on hold and returned to the source account. This process can take anywhere from 3 to 5 days, depending on the bank’s procedures. Given that wire transfers are often booked with specific exchange rates, any delay means missing the initial booking window. Consequently, the entire transaction could be subject to new, potentially less favourable exchange rates once the funds are correctly sourced from the remitter’s account. This scenario is especially critical in time-sensitive payments, such as university fee transfers.

Solution: Funds must come from the remitter’s account.

Robint advises, “Always ensure the transaction is initiated from the account of the person whose KYC documents have been submitted. By adhering to this principle, you eliminate the risk of unnecessary delays and ensure compliance with financial regulations.”

4. Beneficiary Name Mismatch

To ensure a smooth transfer process, it’s important that the beneficiary’s name is consistent across all documents. Any mismatch between the name on the beneficiary’s overseas bank account and the name as it appears on their passport or the A2 Form (the application form for transferring money abroad) can lead to delays or even rejections of the transfer.

Consequence:

- Slight delay – In the best-case scenario, a mismatch in the beneficiary’s name causes the beneficiary or intermediary bank to raise a query for the same to the remitting bank in India. Once the query is resolved the funds will get credited to the beneficiary’s account abroad. This can lead to a short delay in the beneficiary receiving the funds.

- Severe delay – If resolving the name discrepancy takes time, or if there is back-and-forth communication needed between the beneficiary bank, the intermediary bank, and the remitting bank, this can result in a significant delay. The funds might be held up until the correct beneficiary name is confirmed and the transaction is resumed.

- Transaction rejection + high monetary loss + severe delay – In the worst-case scenario, if the beneficiary bank rejects the transaction, the beneficiary bank will send the funds back. This will be again routed via the intermediary bank incurring a $40 fee. Converting the returned funds to Indian rupees at the inward remittance rate results in a 3 to 4% loss compared to the outward rate. To reattempt the transfer, the remitter has to again pay the $40 intermediary fee. This leads to significant financial loss from double fees and currency conversion, plus a considerable delay.

Solution: Ensure correct beneficiary name in Form A2.

Provide the correct beneficiary account name. In case of any discrepancies, provide to the remitting bank in India supporting proofs such as beneficiary passport copy, and the beneficiary’s abroad bank statement containing their correct name. The remitting bank will communicate with the intermediary bank and the beneficiary bank providing these documents to resolve the issue.

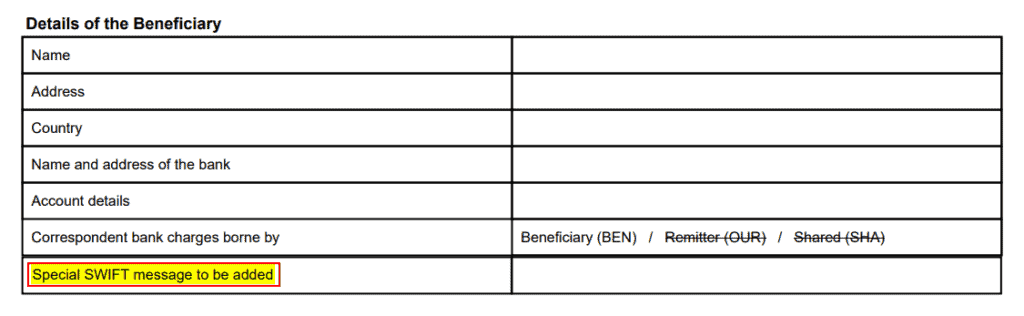

5. Not Adding Specific Identifiers in Form A2 (Special Instructions)

When completing Form A2 for international transfers, especially for educational payments, it’s important to include specific identifiers. Universities often provide special instructions to the student which they must add to their Form A2 in the “Special SWIFT message” row.

This is because, during admissions, a university would be receiving payments from hundreds, if not thousands of students. The special instructions in the SWIFT (unique to each student) helps the university easily identify the student responsible for the payment.

Consequence: Transaction slightly delayed at Beneficiary bank’s end.

Failing to add this information can lead to confusion at the receiving end. The university might not be able to determine who sent the payment, causing delays of maybe 2 to 3 days.

Solution: Don’t forget to add special instructions (if any) at the time of Form A2 filling.

To ensure smooth processing, always include any special instructions or identifiers, like student ID, as specified by the university, in the Form A2. If this step was missed, you might find yourself needing to provide additional proof of payment, such as a SWIFT copy, to help resolve any identification issues with the university.

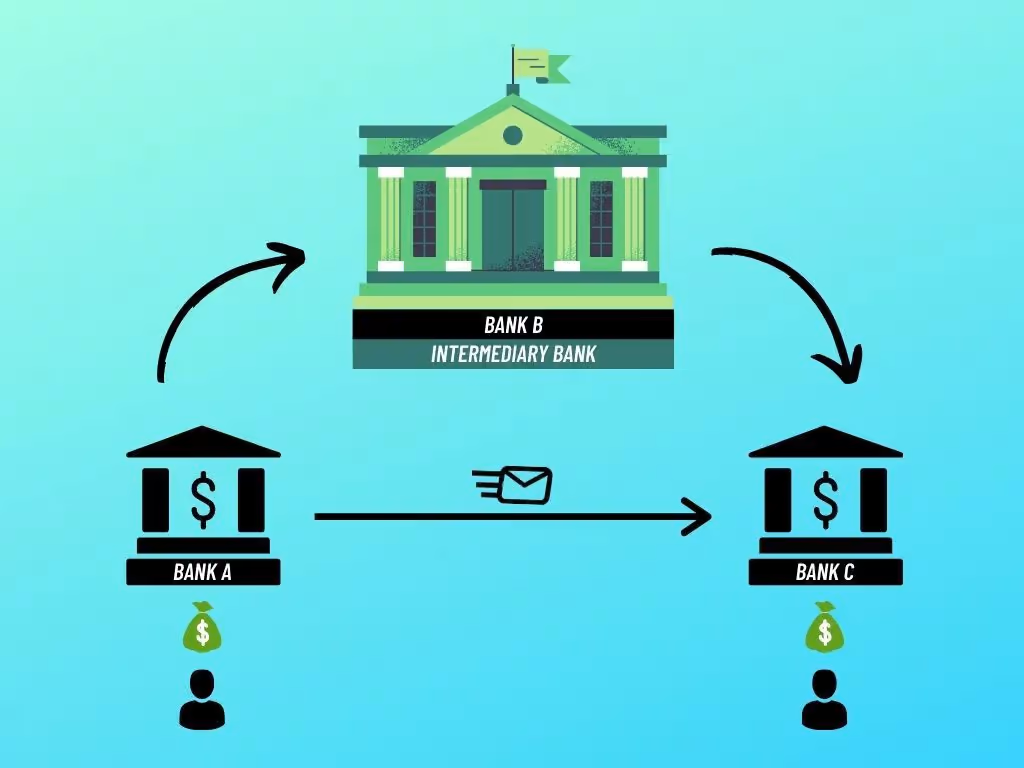

6. Not Factoring in Intermediary & Beneficiary Bank Charges

Overlooking intermediary and beneficiary bank charges is a common mistake that can significantly impact the amount your recipient ultimately receives.

A remittance transaction from India to another country often passes through an intermediary bank(s). They mostly charge a fee of up to USD 40 equivalent to route the funds. Thereafter the funds will be sent to the recipient’s bank (beneficiary bank), which might also impose a fee for accepting international funds (this happens only rarely).

If you have not factored in these charges, the beneficiary will receive a lesser amount than what you intended.

Consequence: Beneficiary receives less money. Worst case scenario – Transaction rejection + high monetary loss + severe delay.

For personal remittances, the main impact is simply receiving less money than expected. However, the stakes are higher for transactions like university fee payments, opening GIC/Blocked Accounts, or fulfilling conditions for university enrollment (confirming your seat at a foreign university). Receiving insufficient funds can lead to the outright rejection of the payment.

Universities, for instance, will not negotiate on initial payments for conditional enrollment; if the full amount isn’t received, the transaction could be rejected and refunded, which is a process that could take 5 to 7 working days. The refund will also be subject to intermediary charges and converted at a less favourable rate, further reducing the amount returned to the remitter. This not only results in financial loss but also wastes precious time, potentially jeopardizing university admissions within strict timelines.

Solution: Check beforehand about Intermediary & Beneficiary fees and add a buffer amount

Robint advises “To prevent these issues, consult with your remitting bank about any intermediary fees and have the recipient inquire about incoming fees at their bank. Based on this information, add an appropriate buffer to the amount being sent to cover these additional charges.” This ensures the correct amount arrives at its destination, avoiding delays, rejections, and the need for costly re-transmissions.

7. Choosing The Wrong Transfer Option

Selecting the appropriate option for covering intermediary charges is critical in international money transfers. The choice between BEN (Beneficiary Pays), OUR (Sender Pays), and SHA (Shared Costs) has a direct impact on the amount the recipient receives.

Consequence: Beneficiary receives less money. Worst case scenario – Transaction rejection + high monetary loss + severe delay.

Intermediary fees would end up being deducted from the transferred funds depending on the “Transfer Option” chosen. The beneficiary will receive less funds than expected. This can sometimes lead to transaction rejection (overseas education-related transfers). As you know from the previous points, a transaction rejection means a lot of monetary loss for the remitter. Intermediary fees would be again levied during the refund (USD 40 equivalent). Also, inward remittance exchange rates would apply leading to a loss of 3 to 4%. On top of all this monetary loss, your time would also be wasted because of the delays experienced.

Solution: Always verify the “transfer option” selected on your A2 Form.

- If Choosing BEN – The intermediary fees would be deducted from the amount being transferred. Make sure to enquire about the intermediary fees applicable and add that amount as an additional buffer on top of the amount you want to send. If any deductions happen, it won’t affect the amount of money that the beneficiary has to receive.

- If Choosing OUR – You pay for the intermediary fees upfront to the remitting bank so that no further deductions happen along the way. Also, check with the beneficiary if their bank would deduct any amount for receiving the funds.

- If Choosing SHA – Some part of the intermediary charge will have to be paid upfront by the remitter. The rest will be deducted from the funds being transferred. Since there is less clarity about the sharing of the intermediary costs between the remitter and the beneficiary it is best not to go for this option. Usually, banks will recommend you either choose between either BEN or OUR.

Also Read: Intermediary Bank Charge Fully Explained

8. Entering Incorrect Beneficiary Bank Account Details

Robint elaborates on this point, “Sometimes the sender enters incorrect beneficiary account details. When you are reading the account number from somewhere else, maybe from the beneficiary’s WhatsApp message and inputting it in Form A2, mistakes can be made. This seemingly small oversight can have significant repercussions”.

Consequence: Best case scenario – Transaction delayed, Worst case scenario – Transaction delayed + financial loss.

- Funds stuck at intermediary bank: If the entered bank account number does not exist, the funds are likely to be halted at the intermediary bank, which will then contact the remitting bank for correct details.

- Funds credited to the wrong account – On the other hand, if the incorrect account number belongs to an actual account and there’s a significant match in details, the funds might mistakenly be credited to the wrong account. Resolving such issues involves communication between the sending bank and the beneficiary’s bank to reverse the transaction. This process incurs intermediary bank charges and the remitter may receive a lesser amount due to the application of inward remittance rates during the refund. The end result is not just financial loss but also significant delays, requiring the transaction to be initiated all over again with the correct account details.

Solution: Double-check the beneficiary’s bank account details before submitting the A2 Form. If you discover an error after submitting the transfer, act quickly by informing the remitting bank to start the correction process.

Robint has one final piece of advice to share “Successful money transfers are not just about avoiding mistakes but in choosing an expert remittance partner. For those looking to bypass these complications altogether, ExTravelMoney offers a seamless solution.”

By booking your remittance transaction with us, you’re opting for a service that not only helps you avoid all money transfer-related headaches but does it for you while providing excellent exchange rates, helping you save your valuable money too. Our promise of a hassle-free and value-for-money experience is backed by outstanding reviews on Google and Trustpilot. Trust in ExTravelMoney for professional, seamless money transfers.

Also Read: How Wire Transfer From India to Abroad Actually Works

Subhash, with over 10 years of experience as a content writer in the finance niche, is the head of content at ExTravelMoney.com. His expertise spans international remittance, currency exchange, RBI regulations, and travel abroad, simplifying complex financial topics, and transforming them into accessible and engaging content.