Have you ever thought about how money is transferred from India to another country? If your answer is yes, then this post is for you!

Money Transfer has come a long way from physically needing to transport currency notes and coins in armoured trucks or trains (and fending off robbery attempts on the journey!).

Nowadays, at the click of a button, the same is possible electronically simply by passing messages between banks (Wire Transfer)!

Here we’ll discuss the juicy and interesting details of how International Money Transfer from India takes place in modern times.

International Money Transfer (Wire Transfer) From India to Abroad via Banks

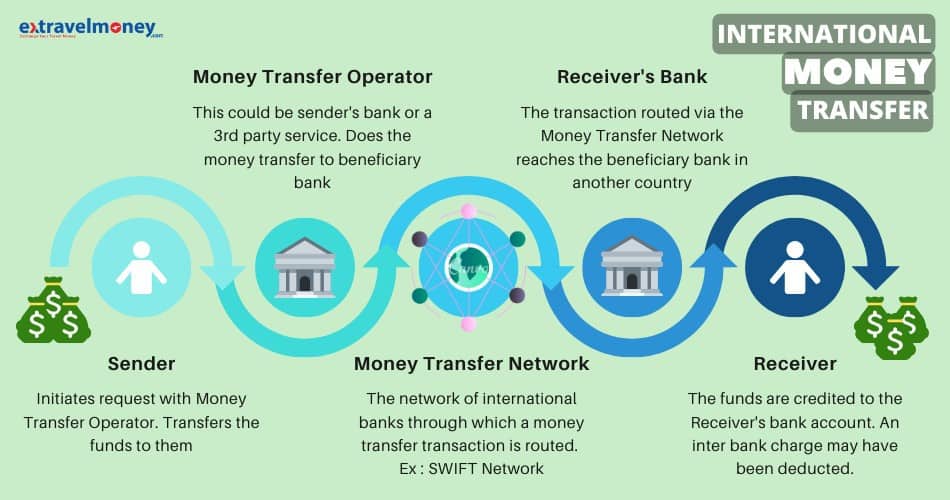

Banks in India and the world over use what is called “Wire Transfer/Telegraphic Transfer” to send money abroad.

The first Wire Transfer took place back in 1872. It was done by Western Union through their own Telegraph network. The sender paid the money to the Telegraph operator in their town, who then sent a telegraph message to the recipient’s town instructing the release of funds to the recipient.

Even now, this same principle is followed by banks to move money hence it’s also known as the Telegraphic Transfer.

Take a look below at the 5 steps of “Wire Transfer” to move funds internationally;

1. The sender chooses a money transfer service provider

A money transfer service is not only performed by a bank but it can also be done by a third-party service provider known as a money changer. So there are a lot of options to choose from.

For example: In a country like India there are many banks which do money transfers abroad like HDFC, ICICI, SBI, PNB, RBL Bank, Axis Bank etc.

Apart from them, there are also authorized money changers who can provide the same service such as Thomas Cook, UAE Exchange (now Unimoni).

2. The service provider does KYC documents verification

The sender’s KYC documents are verified by the money transfer service provider. This is to ensure the sender is following all the RBI remittance rules, especially concerning the maximum allowed limit to remit money abroad (USD 2,50,000 per year).

| What are the KYC documents you need for an international money transfer? You can find the KYC documents required for the different RBI approved purposes of money transfer in the link below; Typically PAN Card, Form A2 (where beneficiary details are filled) and another Govt. ID like Aadhar Card/Driver’s Licence are needed. |

3. The sender transfers the money to the service provider

Once the documents are verified, the remittance transaction is confirmed by the chosen bank or money changer. The sender then has to transfer the money to them via NEFT/RTGS. For this, they’d have to add the money transfer service provider as a beneficiary. Once this is done, the sender sends them the money.

What are the fees for doing a “Wire Transfer” from India to abroad?

|

4. The service provider initiates the “Wire Transfer” message over SWIFTNet Network

The exchange rates are booked and the beneficiary information is fed into the SWIFTNet Network.

SWIFT stands for Society for Worldwide Interbank Financial Telecommunication. It was developed in 1973 as a standardized way for banks to coordinate financial transactions and data exchange around the world electronically. A software (SWIFTNet Link) is provided to the banks in the SWIFTNet Network through which the international money transfer transactions are carried out.

If the sender’s bank and the receiver’s bank have a direct relationship under SWIFT, then the transaction is processed speedily.

However, if the sender’s bank doesn’t have a direct relationship with the receiver’s bank then there may be a delay in transaction completion.

In such a case, a network of intermediary banks in SWIFT, which have connections to both the sender and receiver bank, comes to the rescue. The SWIFT message is routed through them (thus the delay) and finally, the message is transmitted to the receiver’s bank.

Overall, a Wire Transfer may take anywhere between a few hours to 2 working days to get processed and this is one of the main drawbacks of SWIFT.

On the other hand, SWIFT transfers are one of the safest ways to send money internationally from India and are approved by RBI.

5. The beneficiary bank receives the Wire Transfer message and credits the funds to the beneficiary account

So finally, after all these processes, the receiver’s bank gets the Wire Transfer message and releases the funds to the beneficiary bank account.

In all these steps there is never a physical movement of money from one location to another. What is happening is banks passing messages to move the money virtually through the use of electronic messages over the SWIFTNet network (and an electronic ledger maintained by different banks recording the virtual movement of money).

Pretty fascinating, isn’t it?

Also Read: What Is IBAN Number and Why You Need It To Transfer Money Abroad?

Subhash, with over 10 years of experience as a content writer in the finance niche, is the head of content at ExTravelMoney.com. His expertise spans international remittance, currency exchange, RBI regulations, and travel abroad, simplifying complex financial topics, and transforming them into accessible and engaging content.