While doing a Wire Transfer abroad, you might have come across the terms “Intermediary Charge” and “Beneficiary Bank Charge”.

So what exactly do these terms mean?

Intermediary Bank Charge is the amount charged by a 3rd party bank(s) that act as a go-between, to facilitate a money transfer transaction between two different banks. The 3rd party bank(s) receiving funds from the sender’s bank and routing it to the beneficiary’s bank is known as the Intermediary Bank. This charge is almost always applicable on all money transfer transactions abroad. The sender’s bank will be not be knowing about the exact charge beforehand. It is usually around US $15-30.

The beneficiary bank abroad may charge an amount for receiving money. This is called the Beneficiary Bank Charge. The sender’s bank cannot say beforehand if such a charge will be applicable on a particular transaction. This is because the Beneficiary Bank Charge is decided by the Beneficiary Bank. It can range anywhere from US $0-15.

So now you’d be thinking, why is an Intermediary bank required to facilitate the transaction between two banks? Why can’t the two banks directly transfer money to each other?

This is because for two banks to transfer money to each other directly, they must have a direct financial relationship with each other. If not, then intermediary banks come into the play to complete the transaction and in return for their service collect a flat fee known as the Intermediary Bank Charge.

Example:

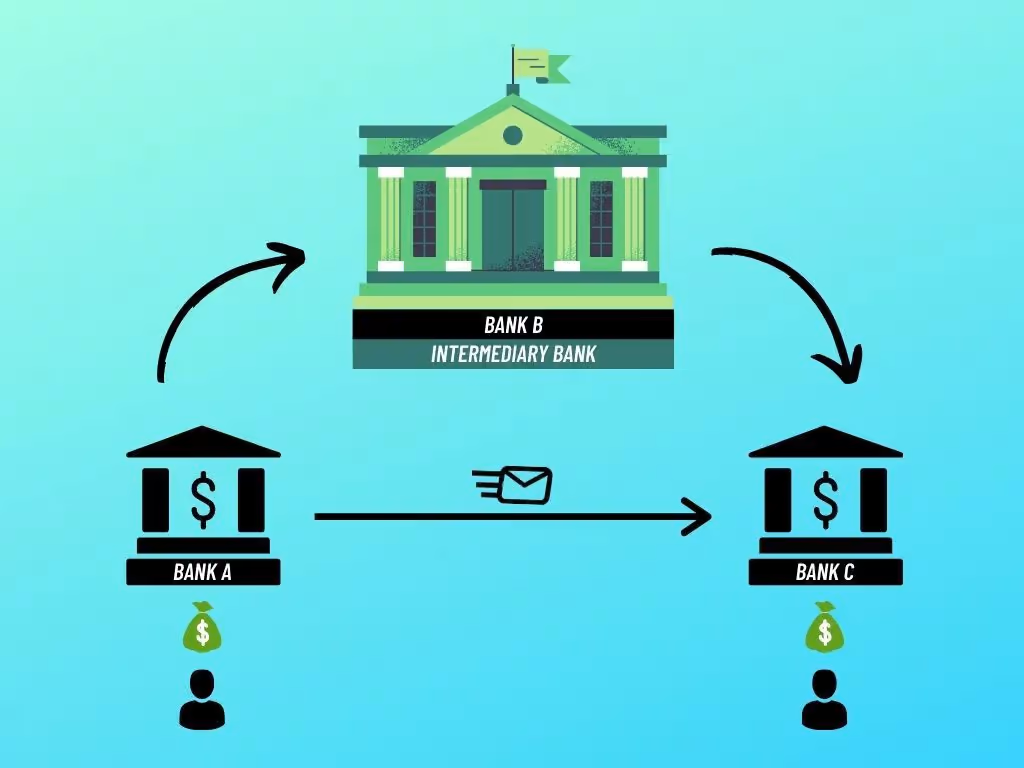

The sender from Bank A wants to remit money to the Beneficiary in Bank C. However, both these banks do not have a direct connection in the Wire Transfer Network but are respectively connected to Bank B.Thus when a wire transfer is initiated from Bank A to C, the funds will be routed through Bank B which will facilitate this transaction and in return charge an amount which is known as the intermediary bank charge. |

Usually, Intermediary Banks are required in outward remittance transactions, when two banks in different countries don’t have any prevailing financial relationship.

How does money transfer take place between two different banks?

There is no physical movement of cash involved when one bank transfers money to another.

Instead, the mechanism that makes this happen is called a Correspondent account/Nostro account.

A bank must hold a correspondent account with another bank to transfer money to them directly.

One drawback of this method is that it not possible for a bank to hold a correspondent account with a large number of banks across the world.

Also Read: How Wire Transfer From India to Abroad Actually Works

What is the role of an intermediary bank in an international money transfer?

SWIFT is the de-facto cross-border payments network used by more than 11000 banks across 200+ countries in the world.

In a SWIFT transfer (also known as “Wire Transfer/Telegraphic Transfer), banks do not transfer funds to each other. Instead, a message called a payment order is generated from one bank to another.

If the sender’s bank has a correspondent bank account with the receiver’s bank, then the transfer happens directly. Funds to the beneficiary are settled from the correspondent account of the sender’s bank.

However, SWIFT being such a huge network of banks, most of the banks usually don’t have a direct financial relationship with each other.

That’s when an Intermediary bank is used to complete the transaction.

The payment order generated by the sender’s bank passes through an intermediary bank or through multiple intermediaries before reaching the beneficiary bank.

The SWIFT network automatically optimises the transfer to take the minimum number of steps required to complete the transaction.

The intermediary banks also verify the transaction by performing checks to ensure it is not facilitating illegal activities or money laundering etc.

What are the beneficiary details required to initiate a SWIFT transfer?

This could be Transit code (Canada), Sort code (UK), IBAN (Middle East), BSB Code (Australia) |

Why is the Intermediary Bank Charge also known as Beneficiary Bank Charge?

When sending money abroad using the SWIFT network, the sender has the option to choose who gets to pay the Intermediary bank charge & Beneficiary Bank Charge.

It can either be the sender or the beneficiary. In all SWIFT transactions, the bank must indicate in their SWIFT message from whom the charges are to be collected (after consulting with the sender). This is denoted by 3 terms;

- OUR – Sender pre-pays the intermediary bank charge to their bank and the beneficiary bank charges (if any) would be debited from the transferred amount (borne by the beneficiary)

- SHA – Sender and beneficiary agree to share the intermediary bank charge. The sender pre-pays half of the charge to their bank. The Beneficiary’s share of intermediate bank charge and beneficiary bank charges (if any) would be debited from the transferred amount (borne by the beneficiary)

- BEN – Intermediary Bank Charge and Beneficiary Bank Charge (if any) would be debited from the transferred amount (borne by the beneficiary).

If a sender chooses the 3rd option, then the intermediary bank charge and the beneficiary bank charge are together charged by the beneficiary bank.

Since in most transactions, the sender always chooses the BEN option, the intermediary bank charge and beneficiary bank charge came to be collectively known as the beneficiary bank charge.

The beneficiary bank then pays the intermediary bank charge to the intermediary bank.

How much are the intermediary/beneficiary bank charges for money transfers abroad from India?

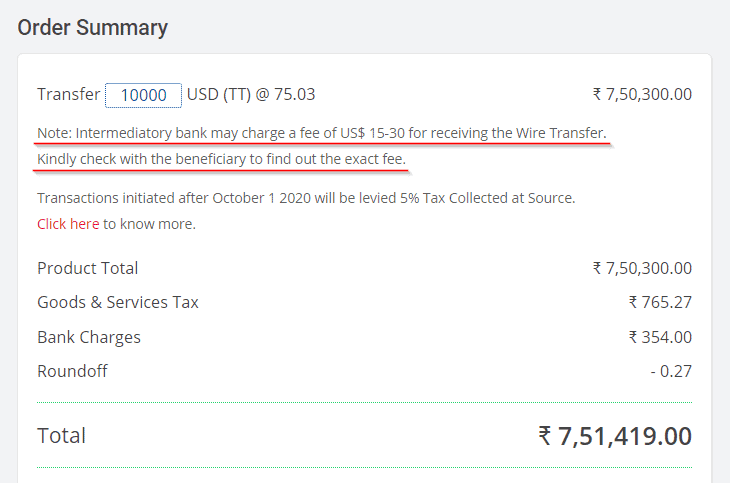

The above image is a quote for transferring 10,000 USD from India to abroad (as on 02/11/2020).

Typically, the intermediary bank fee is in the range US$ 15-30 or its equivalent in other currencies. That is roughly about Rs 1,118 to Rs 2,235.

What are the different ways to pay the Intermediary Bank Fees?

As per the SWIFT Standard field 71A “Details of Charges”, there are 3 ways to pay the Intermediary Bank Fees.

- OUR – If “OUR” is indicated in the SWIFT payment message, it means the sender will be pre-paying the fee of the intermediary bank(s). The intermediary fee (Usually US$ 15-30) will be collected by the sender’s bank and it’ll be the one responsible for settling the intermediary fees with the 3rd party banks. The intermediary banks won’t collect their fees from the amount being transferred. It’ll be deposited as it is to the beneficiary account. However, there is a drawback of using “OUR”. Under the SWIFT network, it’s not possible to know beforehand who the intermediary bank(s) will be and how much will be the charge. Usually, for transfers below US$ 1,000, the intermediary fees are commonly in the range of US$ 10-15. In fact, sometimes there won’t be any intermediary charges also. In such a case, if the sender opts for “OUR” and pre-pays the intermediary bank fees to the sending bank (US$ 15-30), sometimes those funds may be underutilized or not used at all. Whatever balance of this amount is remaining the sending bank will pocket it.

- SHA – When “SHA” is marked in the SWIFT payment message, it means the sender will pre-pay for half the intermediary bank charge to the sending bank. The sending bank will pay this half to the Intermediary bank. The beneficiary would have to pay for the rest half of the “intermediary bank charge”. The intermediary bank will collect this half-charge from the amount being transferred.

- BEN – “BEN” refers to the beneficiary bearing the cost of both intermediary fees. For example: When sending 10,000 USD abroad, say intermediary bank charge is $15. The intermediary bank will collect their fees of $15 from the amount being sent. Finally, $9,985 will be credited to the beneficiary account abroad.

In case of personal transfers to say your loved ones abroad like son or daughter studying there or relatives, we always recommend using “BEN”.

Customers can add the intermediary bank charge and beneficiary bank charge on top of the amount being sent (to be on the safe side) and do the transfer.

|

For Example; Assume Intermediary Bank Charge – $15, Beneficiary Bank Charge – US $0 to US $15. Instead of sending exactly US $10,000, the sender sends $10,030 and chooses option BEN. Intermediary Bank Charge $15 and Beneficiary Bank Charge $15 are collected from the transferred funds by the beneficiary bank. Now the beneficiary won’t be inconvenienced by receiving a lesser amount as they get exactly US $10,000 even after the deductions. Also, if no beneficiary bank charges apply (US $0), they’d get to keep those extra $15 and your close one would get more money than they expected. Also, in some rare cases, sometimes no intermediary bank charge may be levied. In that case, the beneficiary would get to keep $30 extra. |

Now that you’ve got a deeper understanding regarding the nature of SWIFT transfers and the role of intermediaries, you now know why intermediary bank charges are applied on money transfers abroad.

Please feel free to add your comments or questions below.

Also Read: What Is IBAN Number and Why You Need It To Transfer Money Abroad?

Subhash, with over 10 years of experience as a content writer in the finance niche, is the head of content at ExTravelMoney.com. His expertise spans international remittance, currency exchange, RBI regulations, and travel abroad, simplifying complex financial topics, and transforming them into accessible and engaging content.