So you are an NRI who has money saved up in India. Or maybe, you just recently acquired some money by way of a property sale.

Either way, now you want to repatriate these funds from India to the country where you are currently living.

If you are looking to know how much tax you’ve to pay on NRI repatriation, you’ve come to the right place.

In this article, we’ll explain the taxes applicable to different NRI repatriation transactions.

Also Read: How Can NRIs Transfer Money From India – Complete Guide

Disclaimer: This article on tax obligations for NRI repatriation is for informational purposes only and does not intend to be tax advice. Please consult a financial advisor or a tax professional to get personalised guidance on your specific circumstances.

Tax on NRI Repatriation

| Type of NRI Account | Tax on Repatriation |

| 1. NRE: Non-Resident External Account | Only GST; 1. GST on INR to Foreign Currency Conversion 2. GST on service charge |

| 2. NRO: Non-Resident Ordinary Account | Funds in the NRO account are first subject to multiple taxes. Only when these taxes are paid off is repatriation possible; 1. Capital gains tax on money in the NRO account received via investments. 2. Money earned via any salary in India. 3. Money in the NRO account earned via way of rental property income in India. 4. Interest earned on the money lying in the NRO account (TDS at 30%). Once these taxes are paid off, the only tax on repatriation from NRO account is; 1. GST on INR to Foreign Currency Conversion 2. GST on service charge |

| 3. FCNR: Foreign Currency Non-Resident Account | Only GST on service charge |

Note: To find out the exact GST applicable on the amount you want to repatriate from your NRI account, read our blog post below;

How Much Tax You’ve To Pay On Foreign Exchange Transactions In India?

1. NRE Account

A Non-Resident External Account allows NRIs to park their ‘foreign earnings’ in India in ‘Indian Rupees’.

When you are transferring money from abroad in foreign currency into your NRE account, it is converted to INR at the prevailing exchange rate and deposited.

Benefit

- Tax-Free: Money in NRE accounts isn’t taxed. This means you don’t pay any tax on the money you deposit (the principal) or the interest it earns.

- Free to Move Money: You can easily move your money, including the principal and interest, from your NRE account to any foreign account. This process is known as repatriation.

Drawback

- Depreciation of INR w.r.t. Foreign Currencies: At the time of depositing, the foreign currency is converted into INR. However, we know about the trend of INR depreciating against major foreign currencies such as USD, Euro, GPB, AUD, CAD, and Gulf currencies etc. In future, when you try to repatriate from your NRE account you may get a lesser amount of the foreign currency than you deposited initially.

Tax on Repatriation From NRE Account

Only GST is applicable;

1. GST on INR to Foreign Currency Conversion – When repatriating money from your NRE account, the INR in the account is converted to foreign currency. For this, GST is applicable.

2. GST on service charge of the bank/money changer doing the NRE repatriation

3. No TCS

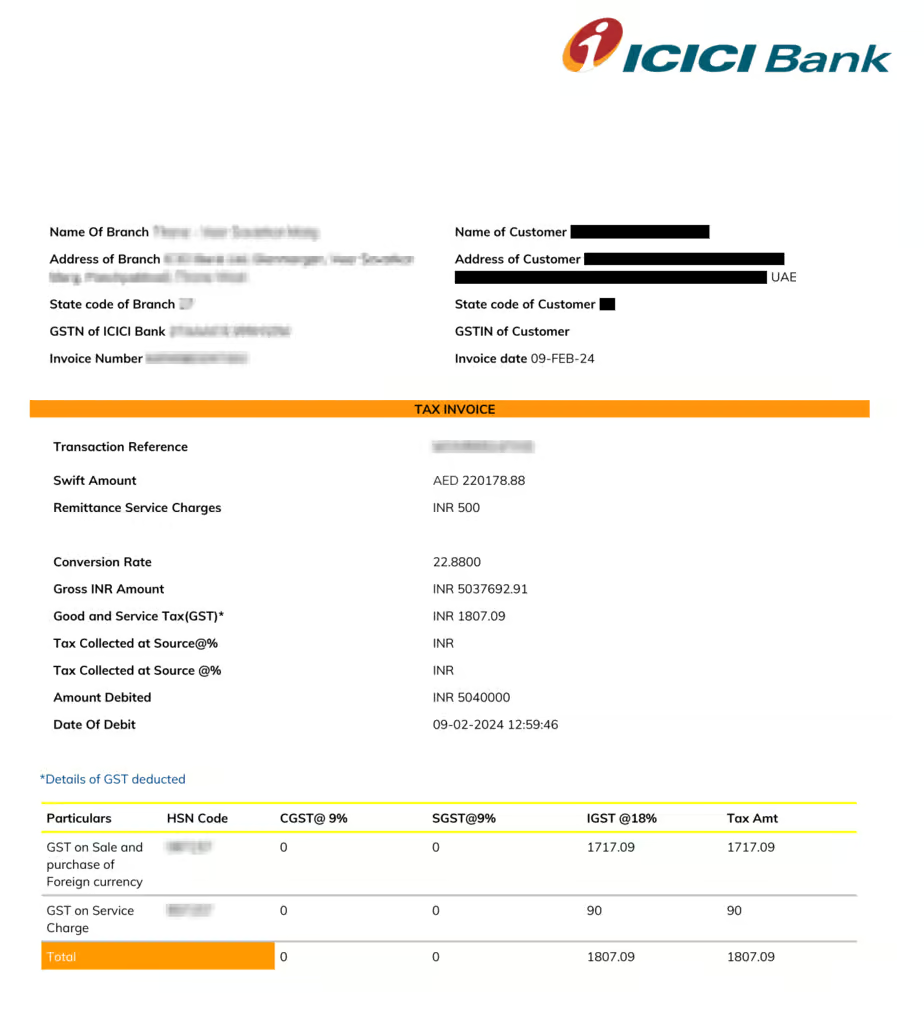

Here is a sample invoice of a customer who did repatriation from their NRE account via ExTravelMoney (ExTravelMoney.com has a direct partnership with ICICI Bank). The invoice also contains the tax details.

Maximum Repatriation Limit

- No Restrictions on Transfer: There are no limits on transferring funds from your NRE account to your foreign account.

2. NRO Account

A Non-Resident Ordinary Account is a very useful way for NRIs to maintain an account in India where they can deposit their ‘Indian earnings’.

The ‘Indian earnings” of NRIs span across various sources. These earnings can be;

- Rental income earned from their properties such a house, or commercial space.

- Dividends from investments such as Mutual Funds or Shares in a company.

- If the NRI is having pension in India, then this would also go to their NRO account.

- Additionally, income from the sale of property, whether it’s a piece of land or a built structure, also falls under ‘Indian earnings’.

Benefit

- Managing Indian Earnings: An NRO Account enables NRIs to effectively manage their India-sourced income.

- Easy Access in India: With an NRO account, NRIs can easily access their funds while in India for expenses or investments. Like resident accounts, NRO accounts offer full Internet banking and ATM access.

Drawback

- Taxation on Interest: The interest you earn from the deposits in your NRO account is subject to 30% Tax Deducted at Source (TDS). This can significantly reduce the net returns from the investments and savings held in the account.

- Restrictions on Repatriation: Repatriation of funds from NRO accounts is possible but comes with certain restrictions. There is a limit on the amount that can be repatriated in a financial year, and such repatriations require adherence to specific procedures and documentation, which can be a hassle for some account holders.

Tax on Repatriation From NRO Account

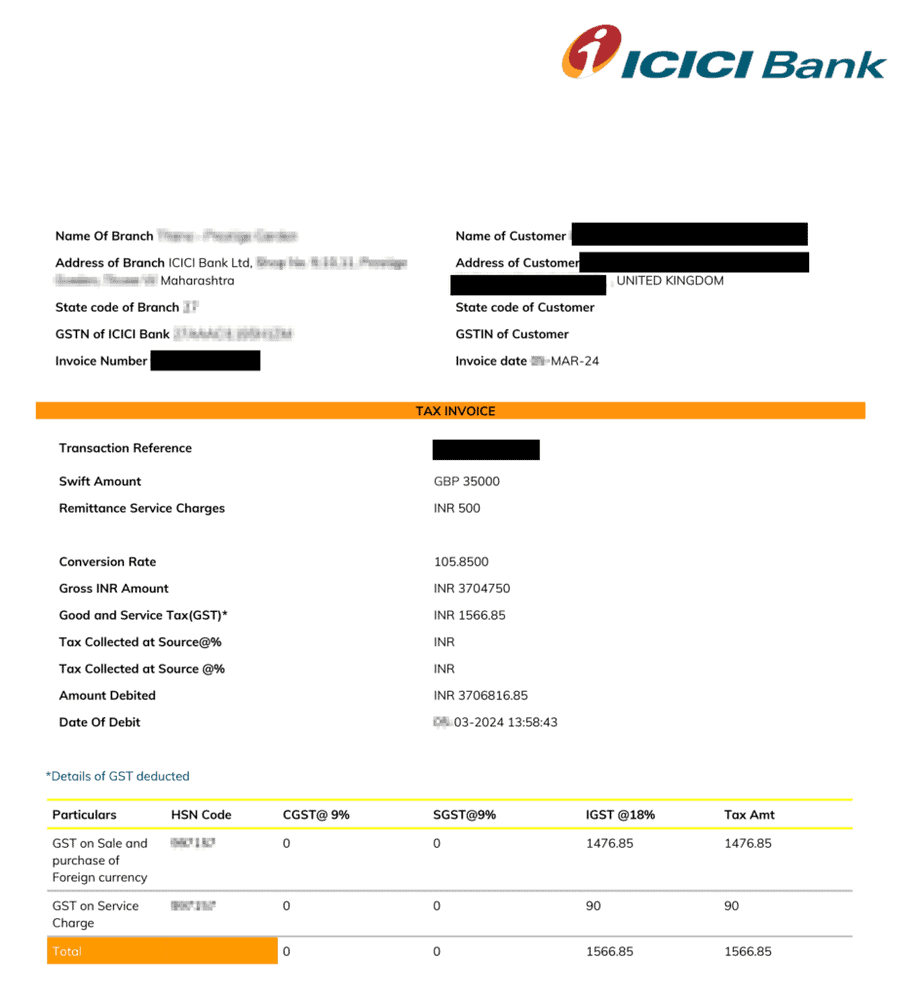

Here is a sample invoice of a customer who did repatriation from their NRO account via ExTravelMoney (ExTravelMoney.com has a direct partnership with ICICI Bank). The invoice also contains the tax details.

- Tax Compliance: Before repatriation, it is mandatory to ensure that all dues and taxes have been paid off in India. The account holder must obtain a Chartered Accountant’s certificate (Form 15CB), which is then submitted along with Form 15CA to the income tax department as proof of tax compliance.

- Only GST Applicable (For conversion from INR to Foreign Currency)

- GST on service charge of the bank/money changer doing the NRE repatriation

- No TCS

Maximum Repatriation Limit

- Annual Limit: USD 1 million. As per RBI rules, NRIs can repatriate up to USD 1 million equivalent per financial year from their NRO account. This limit includes all forms of repatriable funds, including the principal and any accumulated interest.

3. FCNR Account

The Foreign Currency Non-Resident (FCNR) Account is a type of fixed deposit account available in India for NRIs. It enables them to save the money they earned abroad, in foreign currency, in India.

The FCNR account can be opened in various currencies, including US Dollars, Pounds Sterling, Euro, Japanese Yen, Australian Dollars, and Canadian Dollars. This account is mainly for those looking to invest in India while wanting to avoid the risks associated with exchange rate fluctuations.

Benefit

- Hedge Against Exchange Rate Fluctuations: By maintaining savings in foreign currency, account holders are protected against the volatility of currency exchange rates.

- Tax-free Interest Income: The interest earned on FCNR deposits is not taxable in India, providing a tax-efficient investment for NRIs.

- Full Repatriation: Both the principal amount and the interest earned are fully repatriable, meaning they can be transferred without restrictions to the account holder’s country of residence.

Drawback

- Term Deposit Restriction: As FCNR Accounts are term deposits and not savings accounts, they require funds to be locked in for a minimum period. While premature withdrawal is allowed, interest is only payable after completion of one year, potentially reducing liquidity for the account holder.

- Interest Rate Risk: The interest rates for FCNR accounts may vary and are subject to change based on the global financial market, which could affect the returns on the deposits.

Tax on Repatriation From FCNR Account

- Tax-Free Interest: The interest earned on FCNR deposits is exempt from income tax in India.

- No TDS (Tax Deducted at Source): Unlike certain other types of accounts or investments in India, the interest from FCNR accounts does not attract TDS. This ensures that the entire amount of interest earned is available for repatriation.

- No TCS.

Thus there is no tax to be paid to repatriate money from a FCNR Account.

Maximum Repatriation Limit

For FCNR Accounts, there is no maximum repatriation limit. Account holders can fully repatriate both the principal and the interest without any caps, making it a highly flexible option for managing foreign currency funds in India.

Does 20% TCS Apply for NRI Repatriation?

The 20% TCS only applies to foreign remittances under the Liberalised Remittance Scheme (LRS).

However, NRI repatriation of funds from India does not fall under LRS. Thus, it is not subjected to TCS. No TCS is applicable.

Also Read: New TCS Proposals on International Money Transfer in Budget 2025

Avoiding Double Taxation for NRIs

Double taxation refers to the scenario where an individual is taxed by two different countries on the same income.

To prevent such instances, India has entered into Double Taxation Avoidance Agreements (DTAAs) with numerous countries. These agreements allow NRIs to avoid being taxed twice by availing themselves of benefits such as tax credits, exemptions, or reduced rates on the income taxed in India.

NRIs can claim these benefits by providing relevant documents, such as tax residency certificates and Form 10F, to prove their residence status in the treaty country. Additionally, proper disclosure of foreign income in their country of residence is essential to ensure compliance with both local and Indian tax laws, thus effectively avoiding double taxation.

In conclusion, understanding the tax implications of NRI repatriation from India is crucial for effectively managing and transferring funds. The tax treatment varies significantly across different types of accounts, such as NRE, NRO, and FCNR accounts, each designed to cater to the specific needs of the NRI community. While the process may seem daunting, by staying informed and complying with the necessary tax laws and regulations, NRIs can ensure a smooth and efficient repatriation process.

Also Read: NRE vs NRO account for NRIs, What’s the difference & How to choose?

Subhash, with over 10 years of experience as a content writer in the finance niche, is the head of content at ExTravelMoney.com. His expertise spans international remittance, currency exchange, RBI regulations, and travel abroad, simplifying complex financial topics, and transforming them into accessible and engaging content.