If you are coming across this article it’s either because;

1. You’re abroad and want to repatriate money from your Indian bank account.

OR

2. You’re planning a long-term or permanent move abroad and need to know about NRI money transfers from India.

Whether you’re a seasoned expatriate or new to international transfers, this guide simplifies NRI money transfers for you.

| Also, learn how to book NRI money transfers online and at the cheapest exchange rates in India.

Want to get to the good part fast? Click here to scroll down. |

Table of Contents

NRI Money Transfer According to Account Type in India

How to book NRI money transfer online at the cheapest exchange rate

NRI Money Transfer According to Account Type

1. Savings Account

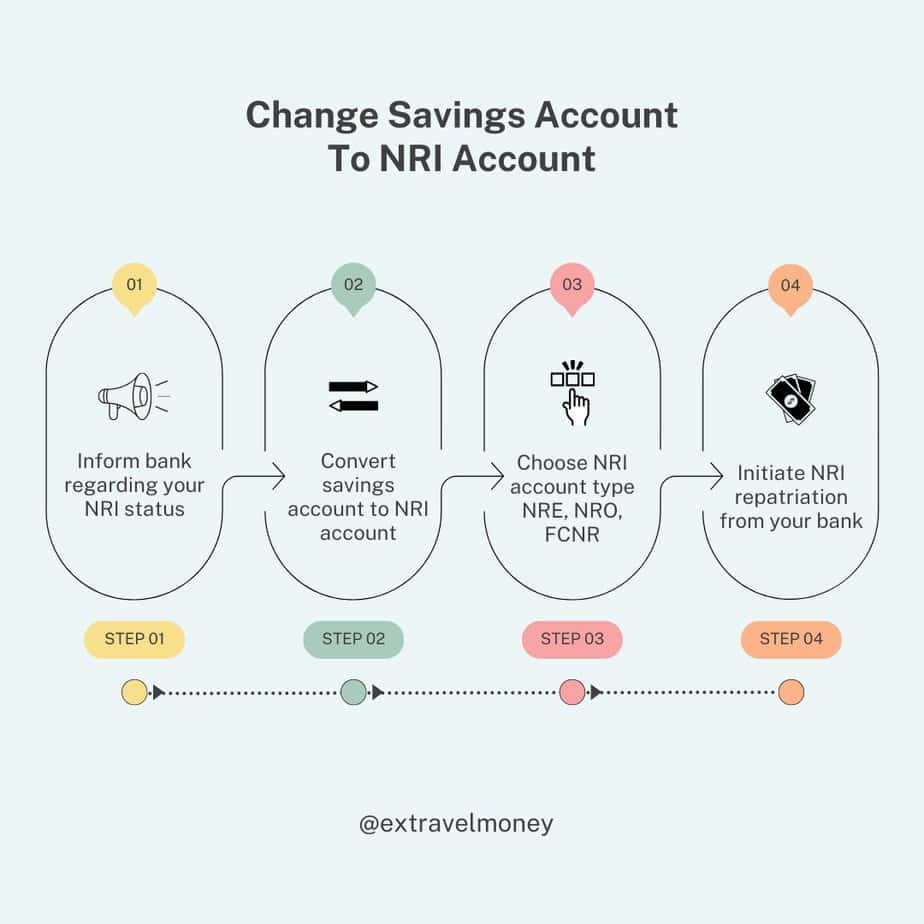

As per RBI rules, NRIs are not allowed to have an Indian savings bank account.

They must convert their existing savings bank account into one of the three NRI account types; NRE, NRO or FCNR.

Thus, if you are going abroad soon, you must inform your bank regarding your impending NRI status. This is to start the process of converting your savings bank account into an NRI account.

RBI does not allow NRIs to do self-remittance from their savings account.

If you have any doubts related to transferring money from a savings account, you can directly whatsapp our NRI repatriation team.

| ☎ +91-9037000696

📧 care@extravelmoney.com |

2. NRE – Non-Resident External Rupee Account

Used for storing your foreign earnings in India in Indian Rupees.

The high point of holding an NRE account is that you can repatriate the entire foreign earnings without any limit. Also, the repatriation process is generally easier than in the case of an NRO account with lesser documentation requirements.

So how to transfer money from your NRE account to your bank account abroad? Let’s take a look.

NRE Account Overseas Money Transfer Process

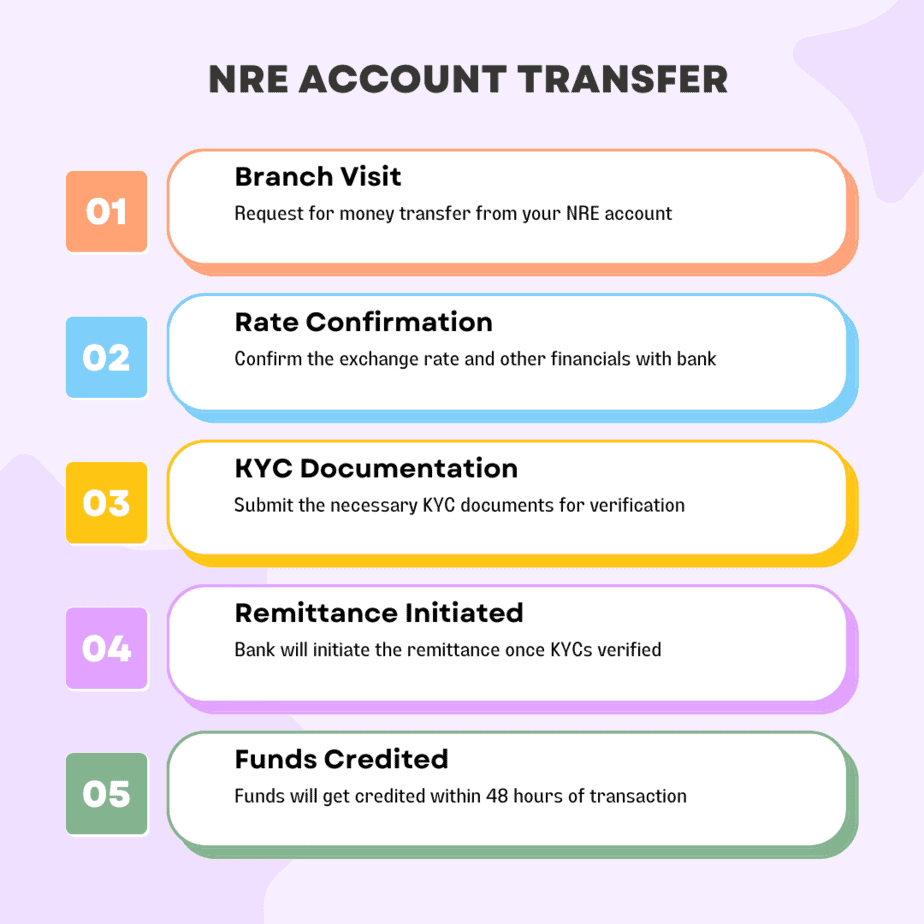

1. Branch Visit

Visit your bank branch and request for money transfer from your NRE account to your foreign bank account.

2. Rate Confirmation

The bank official will detail the conversion rate, service fees, GST, and intermediary bank fee. If you are ok with that, you can confirm the transaction.

Note: Repatriation through banks might cost you a lot as they impose a very high exchange rate. Also, banks charge excessively high service fees.

3. KYC Document Verification

Submit the following documents at your branch for KYC verification;

- Indian Passport

- Visa / PIO (Persons of Indian origin ) / OCI Card (Overseas Citizen of India) – If you are not an Indian citizen

- PAN Card

- A2 form – It’s a form from your bank to specify the remittance amount and foreign bank details. You need to sign it to authorize the money transfer.

4. Transaction Initiation

5. Once the KYC document verification is completed successfully, the bank will initiate the “Wire Transfer/Telegraphic Transfer”.

6. Funds Credited

Funds will get credited within 24 to 48 working hours of transaction initiation. After that, you’ll receive a SWIFT which is proof of your transaction.

3. NRO – Non-Resident Ordinary Account

Used for storing your Indian earnings like rent, pension, dividends, sale of property etc. Since it’s Indian earnings, the amount will be stored in rupees. Any income an NRI earns in India must be deposited in their NRO account.

NRIs can transfer rent, dividends, and pensions from NRO accounts without limits. For non-regular income like property sales, the limit is USD 1 million per year.

Let’s look at how to transfer money from your NRO account to your foreign bank account.

NRO Account Repatriation Process

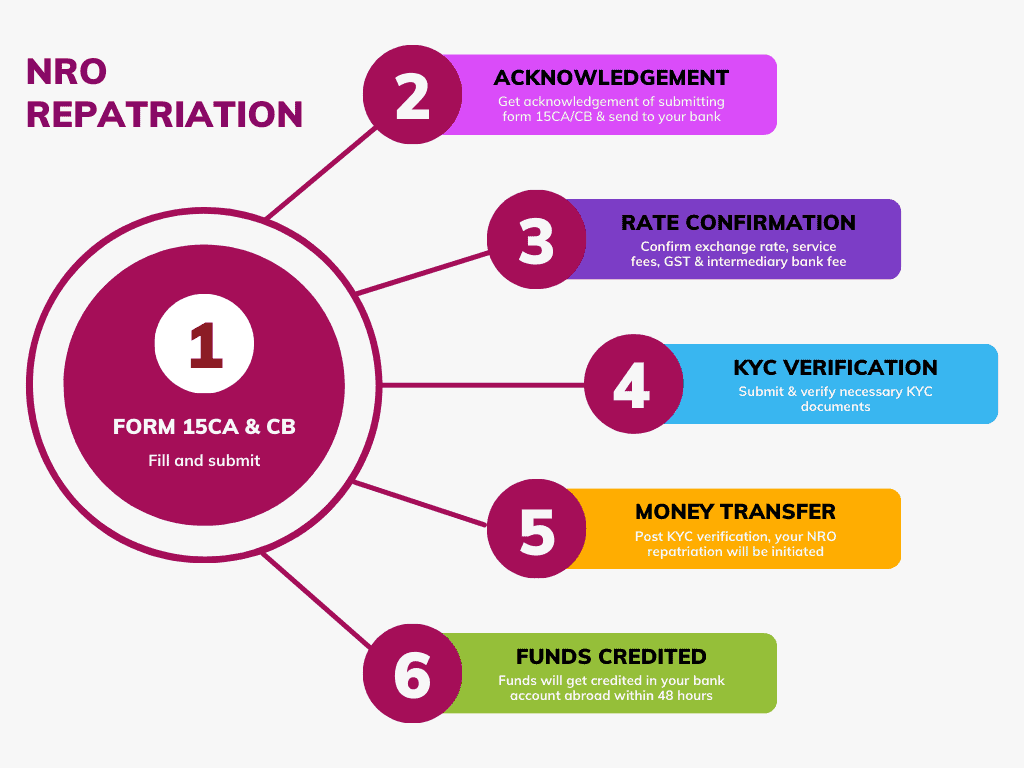

1. Fill & Submit Form 15CA & 15 CB

Form 15CA declares that taxes are paid. It’s for funds remitted from the NRO account.

Form 15CB, issued by a Chartered Accountant, details the remittance purpose and the TDS rate.

You can take the help of a CA in arranging both documents.

| Important Links; |

2. Get Acknowledgement of Form 15CA & 15 CB Submission

After submission of these two documents, an acknowledgement will be received. Then, you need to sign this and submit it to your bank where you hold the NRO account.

3. Rate Confirmation

Confirm the exchange rate, service fees, GST, and intermediary bank fee applicable for the NRO repatriation with your bank.

Note: Using your bank for repatriation purposes can be quite expensive. Banks tend to apply significantly higher exchange rates for NRI transfers. Additionally, the service fees charged by banks are often excessively high.

4. KYC Document Verification

Submit the following documents at your branch for KYC verification;

- Passport of NRI

- Visa / PIO (Persons of Indian origin ) / OCI Card (Overseas Citizen of India) – If you are not an Indian citizen

- PAN Card

- A2 form – It’s a bank form where you enter the remittance amount, foreign bank details, and sign to authorize the transfer.

- 15 CA/CB certificates

- Supporting documents showing the source of funds that is to be repatriated.

For ex: If repatriating the proceeds of the sale of a property, then need to submit a sale deed.

5. Transaction Initiation

After successful KYC verification, your bank will start the money transfer to your foreign account.

6. Funds Credited

Funds will get credited within 24 to 48 working hours of transaction initiation. Afterwards, you’ll receive a SWIFT copy which is proof of your transaction.

Also Read: NRE vs NRO account for NRIs, What’s the difference & How to choose?

4. FCNR – Foreign Currency Non-Resident Account

This NRI account type allows saving foreign earnings in India, in foreign currency, without converting to rupees.

FCNR account is more like a fixed deposit with a tenure ranging from 1 to 5 years. They are a good investment option for NRIs. Since the money is in foreign currency, it is protected from exchange rate fluctuations. Also, the interest earned on the amount is tax-free.

The procedure to repatriate funds from an FCNR account is similar to that of an NRE account.

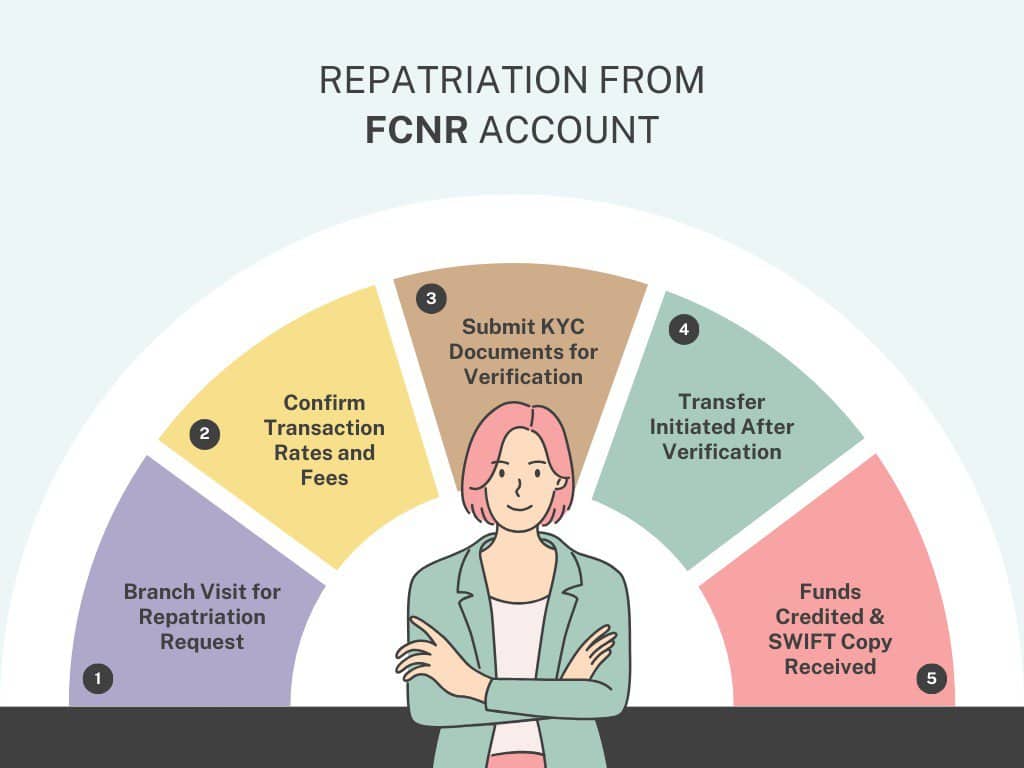

Steps to Repatriate Funds From Your FCNR Account

1. Branch Visit

Visit your bank branch and request for outward repatriation of funds from your FCNR account to your foreign bank account.

2. Rate Confirmation

The bank representative will provide details on their service fees, GST, and intermediary bank fee for the transaction. If these terms are acceptable, you can proceed to confirm the transaction.

Please Note: Repatriating funds through banks can be expensive due to their significantly higher service fees.

3. KYC Document Verification

Submit the following documents at your branch for KYC verification;

- Indian Passport

- Visa / PIO (Persons of Indian origin ) / OCI Card (Overseas Citizen of India) – If you are not an Indian citizen

- PAN Card

- A2 form – It’s a bank form for entering the remittance amount, foreign bank details, and signing to authorize the transfer.

4. Transaction Initiation

Once the verification is completed successfully, the bank will initiate the money transfer from the FCNR account.

5. Funds Credited

Funds will be credited within 24 to 48 working hours after initiating the transaction. Then you will receive a SWIFT copy as proof of the fund transfer.

NRIs can repatriate from NRE, NRO, & FCNR accounts, but NRE or FCNR accounts offer the easiest process. There is no upper transaction limit, you can fully transfer the amount and no taxes will be levied on it.

However, if you have earnings in India, then you need an NRO account to store the money. The NRO account’s downside is its complex repatriation process, making overseas transfers less straightforward.

How to book NRI money transfer online at the cheapest exchange rate

In today’s digital age, transferring money internationally should be as simple as a few clicks. That’s exactly what we offer at ExTravelMoney, especially for NRIs seeking the most cost-effective and convenient way to repatriate funds.

Why Choose ExTravelMoney?

- Competitive Exchange Rates: Our platform offers wholesale exchange rates, typically more favourable than those provided by banks. Customers generally save about Rs 1 to Rs 2 per unit of foreign currency over standard bank rates. This difference adds up, especially for larger transactions.

- Easy Online Booking: Our user-friendly platform allows you to book your money transfer orders online with ease. You can easily compare rates and choose the best option.

- Unparalleled Customer Service: We understand that transferring money abroad can be daunting. That’s why our dedicated team offers personalized guidance every step of the way. From helping you understand the process to ensuring your transaction is smooth and swift, we’re here to assist. Also, our team will guide you through the KYC documentation process.

- Trust and Reliability: At ExTravelMoney.com, we pride ourselves on our transparent and secure services. Thousands of NRIs trust us for their money transfers. We strive to uphold this trust in every transaction.

With ExTravelMoney, it’s about convenience, savings, and peace of mind. Transferring money abroad shouldn’t be a burden.

You can send money for NRI repatriation, family maintenance, investments, or as a gift. Our platform ensures you get the best rates with the best customer service.

Try us out for your next international money transfer and experience the difference.

Frequently Asked Questions

1. Can NRIs maintain a savings account in India?

No, according to RBI guidelines, NRIs are not allowed to maintain regular savings accounts in India. They must convert their existing savings accounts into NRE, NRO, or FCNR accounts.

2. What is the difference between NRE, NRO, and FCNR accounts?

NRE accounts are used for depositing foreign earnings in India in INR. NRO accounts are for managing income earned in India (like rent or dividends). Finally, FCNR accounts are for saving foreign earnings in India in foreign currency.

3. How much money can an NRI repatriate out of India?

An NRI can freely transfer without any upper transaction limit from NRE and FCNR accounts. They can remit up to USD 1 million from NRO account balances for non-current income. However, there’s no limit for current income in NRO account.

4. How does ExTravelMoney.com offer a better solution for money transfers?

ExTravelMoney.com provides competitive wholesale exchange rates, significantly better than typical bank rates. The platform also offers convenience in booking transfers online,

5. Is the money transfer process via ExTravelMoney.com secure?

Yes, ExTravelMoney.com ensures a secure and transparent transaction process, trusted by many NRIs for their money transfer needs.

Also Read: Tax Implications On Money Transferred From Abroad To India

Subhash, with over 10 years of experience as a content writer in the finance niche, is the head of content at ExTravelMoney.com. His expertise spans international remittance, currency exchange, RBI regulations, and travel abroad, simplifying complex financial topics, and transforming them into accessible and engaging content.